- Medicare premiums, deductibles, and out-of-pocket maximums are rising slightly in 2026.

- Costs for many prescription drugs will be significantly lower.

- Medicare Advantage supplemental benefits will be restricted to only those that can have a positive impact on health outcomes.

- Medicare will fully cover all adult vaccines recommended by the Advisory Committee on Immunization Practices (ACIP).

It’s true. Healthcare costs are going up for everyone in 2026, including older adults on Medicare. But there are also some Medicare changes that go into effect on January 1 that will lower costs for some beneficiaries. And there are a number of process and benefit changes that beneficiaries and their family caregivers should be aware of. Understanding these changes in detail can help us better manage and anticipate the financial and healthcare impacts on the people we care for (and on us, TBH).

Below is a comprehensive explanation of the key 2026 Medicare changes, their reasons, and their impact on seniors and family caregivers.

RubyWellTM is committed to helping families navigate the financial journey through caregiving. In addition to providing this helpful information, RubyWell can also predict eligibility for Medicare home health benefits, then guide eligible patients and their family caregivers through the process of accessing that care.

1. Premium and Deductible Changes: What We Need to Know

Part B Premium and Deductible Increase

For 2026, the Medicare Part B standard monthly premium—how much you pay for coverage every month—will increase from $185 to $202.90. That’s nearly a 10% increase. So earmark an additional $215 annually for this.

Part B covers outpatient services like doctor visits, preventive screenings, and medical equipment. Medicare raised the premium to reflect higher healthcare costs overall and expanded use of services by Medicare beneficiaries.

The annual deductible for Part B will also increase from $257 to $283. So our loved ones will need to pay the first $283 of outpatient care costs before Medicare coverage begins. After meeting the deductible, beneficiaries typically pay 20% coinsurance, unless they have a Medicare Supplement (Medigap) plan, which covers the coinsurance portion.

Savings opportunity

Medicare Savings Programs can help low-income Medicare beneficiaries cover these costs.

Part A Inpatient Hospital Deductible Advances

For most people, Medicare Part A, which covers hospital costs, has no monthly premium. But Hospital stays covered under Medicare Part A have an inpatient deductible that beneficiaries pay each benefit period. In 2026, this deductible rises by $60 from $1,676 to $1,736.

A benefit period starts the day our loved one is admitted as an inpatient to a hospital or Medicare‑covered skilled nursing facility (SNF). It ends when they have been out of the hospital and not receiving Medicare‑covered skilled care in an SNF for 60 days in a row. Because benefit periods are not tied to the calendar year, the person we care for can have multiple benefit periods in a single year. And for each one, they have to hit that $1,736 deductible before Medicare starts picking up 80% of the tab.

Savings Opportunity

If the person we care for is homebound, with a high risk of hospitalization, they may be eligible for covered home health services. Studies show that home health care can reduce costly hospital admissions and ER visits. I talk more about this valuable Medicare home health benefit later in this article. So read on.

Part D Prescription Drug Deductible and Out-of-Pocket Cap Rise

Medicare Part D prescription drug plans will also see cost changes. The deductible—the amount our loved one has to pay out of pocket before coverage kicks in—will increase by $25 to a maximum of $615. Additionally, the out-of-pocket spending cap they have to reach before their plan covers 100% of drug costs will rise by $100, from $2,000 to $2,100.

While these increases mean higher upfront costs, they protect our loved ones from catastrophic drug expenses. This is especially true if we care for someone with chronic conditions requiring multiple medications.

Income-Related Monthly Adjustment Amounts (IRMAA)

Medicare beneficiaries with income above a certain limit pay a surcharge (higher premium) for Part B and Part D. That limit is adjusted annually for inflation. For 2026, the starting income threshold for surcharges increases from $106,000 to $109,000 for individual filers. So if the person we care for has an income of $109,000 or higher, their Part B and Part D premiums will be higher than the standard premiums. If our loved one’s income changes significantly after the tax return filing that Medicare used to calculate their surcharges, they can file an appeal.

2. Prescription Drug Coverage: Lower Costs and Convenience

Negotiated Drug Prices for High-Cost Medications

Ready for some good news?

One of the most impactful 2026 Medicare changes comes from the Inflation Reduction Act, which allows Medicare to negotiate prices for certain high-cost drugs. Starting January 1, 2026, ten commonly prescribed medications, including those for arthritis, cancer, and diabetes, will have lower prices. This means that all Medicare Advantage and standalone Part D plans must cover these drugs at the revised prices, making it more affordable for seniors managing multiple chronic conditions at home. All told, Medicare beneficiaries are set to save ~$1.5 billion in out-of-pocket costs in 2026 thanks to this change.

Medicare Prescription Payment Plan (MPPP) Simplifies Payments

The MPPP, introduced last year, will now auto-renew in 2026 beneficiaries who enrolled in 2025 and did not switch plans or actively opt out for 2026. This program allows enrolled patients to spread their prescription drug costs over the calendar year instead of paying lump sums at the pharmacy counter until they hit their deductible. That should help even out a lot of budgets. And automatic renewal means beneficiaries don’t have to re-enroll in it every year. One less thing for us to remember to do! Yo

Affordable Insulin and New Drug Coverage

More good news for those of us caring for someone with diabetes: Medicare will continue capping insulin costs at $35 per month. And a proposed “GLP‑1 pilot” would limit what Medicare beneficiaries pay for certain GLP‑1 drugs like Mounjaro and Ozempic, when they’re prescribed for type 2 diabetes or certain cardiovascular indications. Participants in this pilot would pay no more than about $50 per month out of pocket for a GLP‑1. The pilot could start as early as 2026 but may not be available across all Part D plans.

These additions make it easier for us to keep our loved ones healthy at home, reducing the need for expensive hospitalizations.

3. AI-assisted Prior Authorization

Original Medicare will pilot using artificial intelligence tools to improve the prior authorization process. The pilot will run in six states in 2026: Arizona, New Jersey, Ohio, Oklahoma, Texas, and Washington. And it targets 17 outpatient services that CMS has flagged as overused or vulnerable to fraud and abuse. The hope is that the AI tools will speed up the prior authorization for seniors who legitimately require those services. And they’ll more accurately identify and prevent fraud, waste, and abuse.

4. Medicare Advantage Program: Enhanced Consumer Protections and Coordination

Out-of-Pocket Maximum Update

The maximum out-of-pocket limit for in-network services under Medicare Advantage (MA) plans will slightly decrease in 2026, from $9,350 to $9,250. It’s not a huge reduction. But it’s not an increase either! Most MA plans set caps below the maximum, but this limit provides a critical safety net for those with frequent medical needs.

Strengthened Appeals

Starting in 2026, Medicare Advantage plans have to notify healthcare providers immediately when the plan makes a coverage decision regarding services requested for a patient, while that patient is in the hospital. This new rule also clarifies patients’ rights to appeal coverage denials that impact ongoing treatment.

Refined of Supplemental Benefits

MA plans will have tighter restrictions on what supplemental benefits they can and cannot cover. Simply put, a supplemental benefit must be able to improve or maintain a patient’s health. That means things like non-nutritious food, tobacco products, alcohol, cosmetic procedures, funeral expenses, etc. will not be covered. The goal is to refocus MA plans’ resources on evidence-based services that positively affect health outcomes.

5. Expanded Coverage and Benefits

New Preventive Services

Medicare will fully cover all adult vaccines recommended by the Advisory Committee on Immunization Practices (ACIP). The obvious goal here is to dial up disease prevention and reduce serious illness among seniors.

6. Home Health Care Coverage

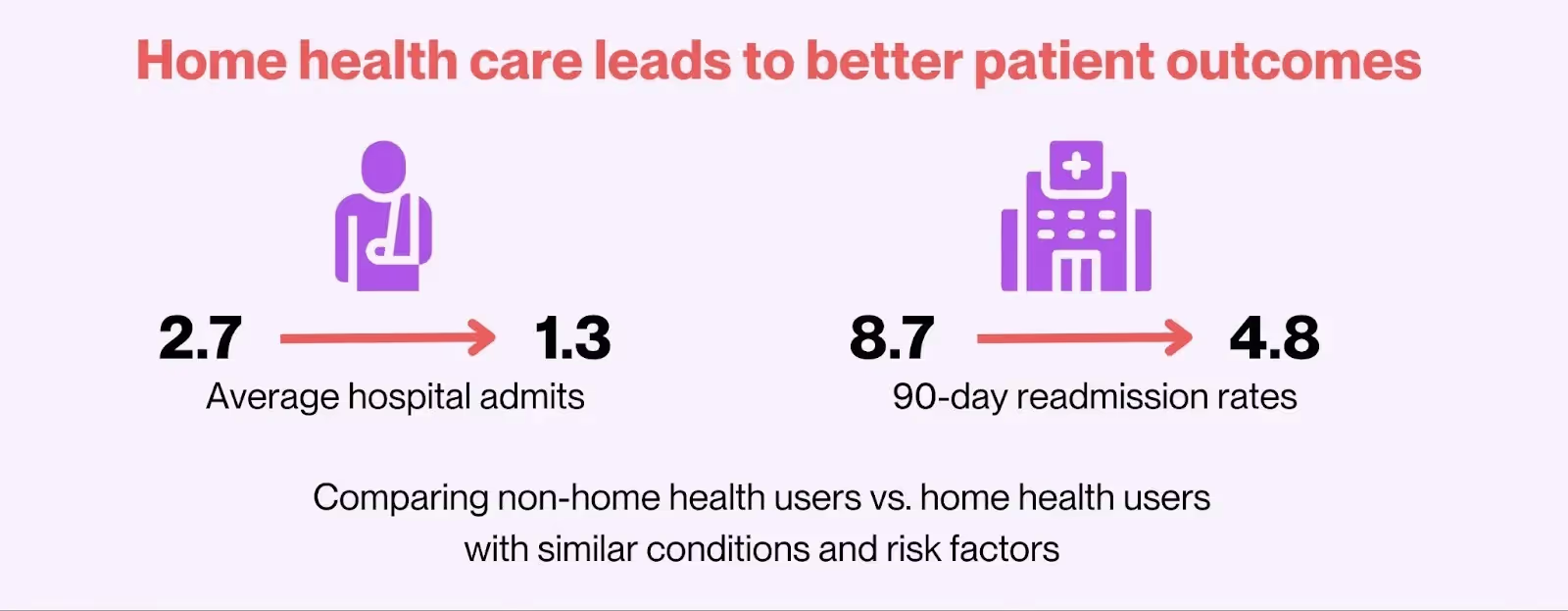

Home health care remains a vital Medicare benefit for our loved ones who are homebound due to physical limitations or medical conditions. Home health services include skilled nursing, physical/occupational/speech therapy, medical social services, and assistance with activities of daily living from home health aides when combined with skilled care.

Medicare data show that patients who receive medically-necessary home health have fewer hospital re-admissions and emergency room visits than patients with similar conditions who don’t receive home health services. And as a family caregiver of two parents who have needed home health, I can say that the services provided really eased the caregiving intensity for my sisters and me.

Source: Evaluation of Home Health Expenditures in a Medicare-Eligible Population

RubyWell’s technology predicts eligibility for the Medicare home health benefit, Then RubyWell representatives guide eligible patients and their family caregivers step-by-step through the process of accessing this valuable care. It all starts with a 10-minute quiz.

2026 Medicare Advantage Enrollment

We just wrapped up the Medicare Advantage Annual Enrollment Period (AEP) on December 7. However the Medicare Advantage Open Enrollment Period (OEP) for 2026 runs from January 1 to March 31. OEP is only for current Medicare Advantage members who want to switch to another MA plan or return to Original Medicare (Parts A and B). They can also add a Part D plan and a Medigap plan at this time.

During OEP, we may only make one change. So we need to do our homework before making a decision. Given all of the 2026 changes, it’s smart to review our loved one’s current coverage and explore new options before the OEP deadline. If we do decide to make a change, the new coverage will go into effect on the first day of the following month.

Note: When switching from MA back to Original Medicare, the Medigap plan providers can underwrite the Medigap policy. This means they can increase the Medigap premium, or even deny coverage, if our loved one has pre-existing conditions. So this could increase costs and limit Medigap plan options. They only times Medigap plans don’t underwrite are:

- When a beneficiary first enrolls in Original Medicare.

- When a beneficiary chooses to switch from an MA plan back to Original Medicare in the first year that they have Medicare Advantage. For example: Our loved one chose an MA plan for the first time with coverage starting on January 1, 2026. In February or March of 2026, they decide they don’t like the MA plan and want to switch back to Original Medicare and add a Medigap plan. In this case, Medigap cannot underwrite their policy.

While we’re reviewing our loved one’s MA coverage, we should pay particular attention to the home health benefits offered by various MA plans versus Original Medicare. While all MA plans must provide at least the same home health benefits as Original Medicare, MA plans can manage those benefits very differently. Many MA plans require prior authorizations, visit caps, narrow networks, and copays, all of which can translate into fewer visits and earlier discharge from home health.

If we do consider making a switch to a new MA plan or Original Medicare, it’s wise to consult our State Health Insurance Assistance Program (SHIP) office. This program offers free, one‑on‑one Medicare counseling to older adults, their families, and caregivers. SHIP counselors are trained, unbiased, and do not sell insurance. So no hard sell there.

What These Changes Mean for Families

Given Medicare’s need to reduce healthcare costs, none of us can really be surprised that the 2026 Medicare updates bring slightly higher premiums and deductibles. At the same time, Medicare is also intent on improving health outcomes. And we can see that in the lower drug costs, smoother payment options, continued insulin caps, and new consumer protections for 2026. So net-net, we may not feel a significant financial impact.

Home health care has also proven to lower costs while improving health outcomes. So for those of us caring for homebound loved ones with chronic conditions that increase their hospital risk, home health could be key to reducing their out of pocket hospital and ER costs. So it’s worth it to check their home health eligibility with RubyWell.

And when I say, “worth it,” I mean worth the time it takes to answer some questions. The eligibility check is free. And the guidance they provide on the journey to access care? Also free. And the home health services they help eligible patients access? Covered by Medicare, so again, free. So absolutely nothing to lose and much to gain.

Here’s to making 2026 a year where managing care feels a little simpler—and where both our loved ones and we, as caregivers, can breathe a little easier knowing help is within reach.

Suzanne Boutilier has been working and writing in the caregiving space since 2021. She also helps her sisters care for their aging father.